How to Determine If You're Financially Ready to Retire

Assessing whether you have enough money to stop working is a critical step for anyone approaching retirement age. While many people turn to simple savings benchmarks as a quick check, financial experts warn that these rules of thumb provide only a rough direction and cannot replace a thorough, individualized plan.

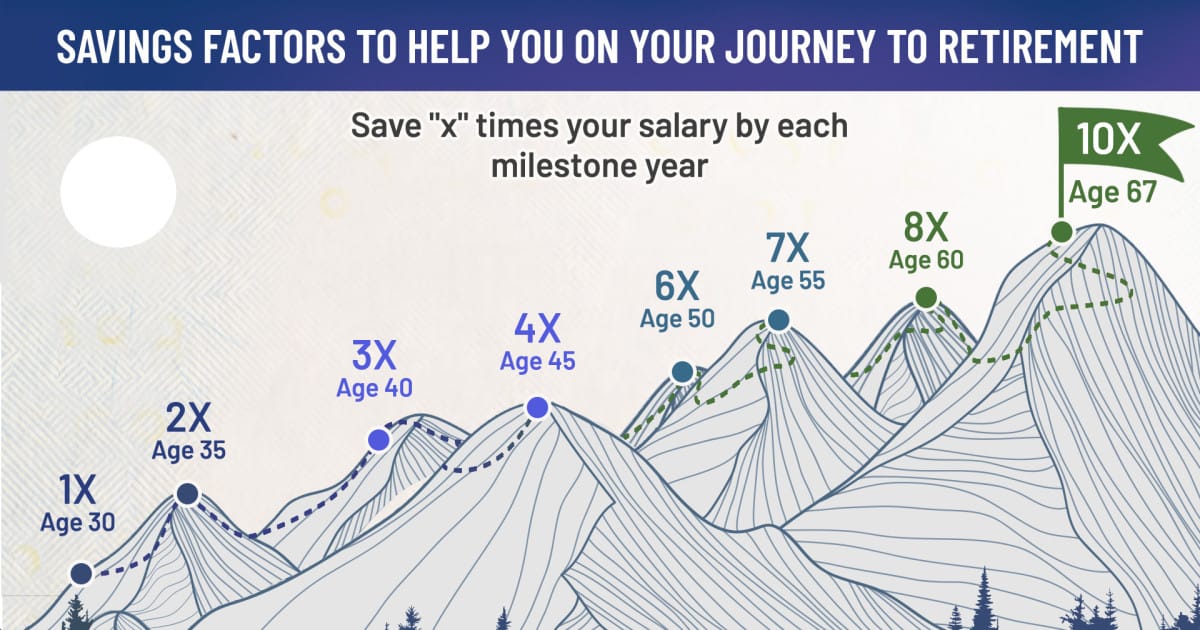

Common benchmarks suggest that retirees should aim to save between 10 and 12 times their final salary or accumulate enough assets to replace roughly 25 percent of their pre‑retirement earnings each year. Such figures can be useful for setting an initial target, but they do not account for variables such as future healthcare costs, regional price differences, or the impact of tax policy on withdrawals. Consequently, relying solely on these numbers may give a false sense of security.

A personalized retirement strategy begins with a detailed estimate of post‑retirement spending. Planners typically model expenses for housing, food, transportation, and discretionary items, then adjust for inflation and the higher likelihood of medical costs as people age. Tax considerations also play a major role; the mix of taxable, tax‑deferred, and tax‑free accounts influences how much income can be drawn each year without triggering unexpected liabilities. Timing of Social Security benefits adds another layer of complexity, as delaying benefits can increase monthly payouts, while early claims reduce them.

The broader context underscores why individualized planning has become essential. In many countries, life expectancy has risen dramatically, meaning retirees may need to fund 30 years or more of living expenses. At the same time, the shift from employer‑provided pensions to defined‑contribution plans places the responsibility for savings and investment decisions squarely on individuals.

Financial advisors generally recommend running multiple scenarios that test different market returns, inflation rates, and spending patterns. Using reputable retirement calculators, individuals can see how changes in contribution levels or withdrawal rates affect the likelihood of outliving their assets. Regular reviews—at least annually—help ensure the plan stays aligned with evolving personal circumstances and economic conditions.

For those uncertain about their readiness, the first step is to gather a complete picture of current assets, projected income sources, and anticipated expenses. From there, a disciplined savings approach combined with periodic professional guidance can increase confidence that retirement will be both financially secure and enjoyable.